25 Aug TOMI: Disrupting the Disinfectant Industry

TOMI Environmental Solutions, Inc. (NASDAQ: TOMZ), is a global bacteria decontamination and infectious disease control company, providing environmental solutions for indoor air and surface decontamination through the manufacturing, sales, service, and licensing of its SteraMist® brand of products, including SteraMist® BIT™, a low percentage hydrogen peroxide-based fog or mist that uses Binary Ionization Technology (BIT™).

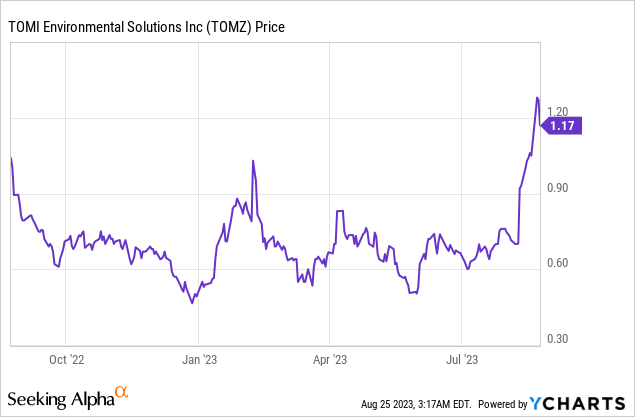

TOMI Environmental Solutions, Inc. (NASDAQ: TOMZ)

Market Cap: $23.19M; Current Share Price: 1.17 USD

Data by YCharts

The Company and its Products

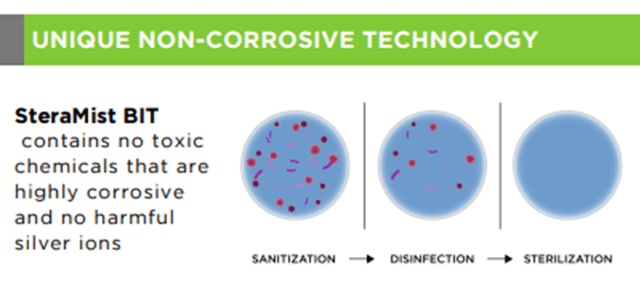

TOMI’s solution and process are environmentally friendly, as oxygen and humidity are the only by-products of the decontamination process. TOMI’s organic solution is listed in Canada as a sustainable green product with no carbon footprint. Most of the Company’s competitors in the disinfection space leave significant by-products and are corrosive. SteraMist is not corrosive, and it does not damage equipment or facilities.

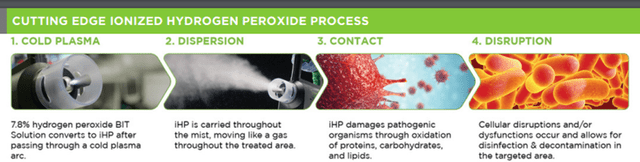

SteraMist® is a patented technology that produces ionized Hydrogen Peroxide (iHP™) using cold plasma science created under a United States Defense Advanced Research Projects Agency (DARPA) grant. The Environmental Protection Agency (EPA) registered BIT™ Solution comprises a low concentration of hydrogen peroxide converted to iHP™ after passing the trade secret blended solution, including its sole active ingredient of 7.8% hydrogen peroxide through an atmospheric cold plasma arc.

iHP™ damages pathogenic organisms by oxidizing proteins, carbohydrates, and lipids. SteraMist® no-touch disinfection and decontamination treat areas mechanically, causing cellular disruptions or dysfunctions resulting in a 6-log (99.9999%) and more significant kill or inactivation of all pathogens in the treatment area.

Image Source: Company

In other words, SteraMist® BIT™ brings to the world a mechanical and automated method of cleaning using a game-changing technology and EPA-registered Hospital-HealthCare disinfectant, providing an upgrade to existing disinfecting and cleaning protocols while limiting liability in a facility when it comes to resistant infectious pathogens. The Company maintains this registration in all fifty states, Washington DC, Canada, and approximately forty other countries that receive this product.

Image Source: Company

Below, we will discuss the critical rationale for covering this Company.

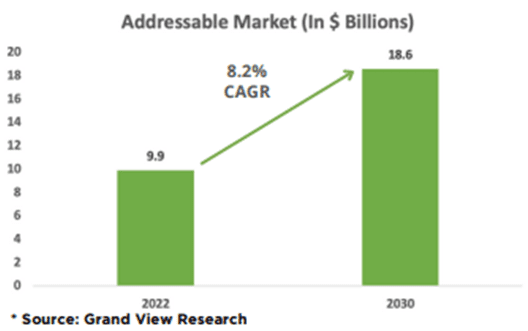

- Expanding Market Demand

Demand for effective disinfection products has grown consistently since 2014 due to the proliferation of hospital-acquired Infections and increasing food safety concerns. Thus, the global disinfectant spray market is expected to grow at a CAGR of 8.2% from $9.9 billion in 2022 to $18.6 billion by 2030.

Image Source: Company

TOMI is expected to benefit significantly from this expanding market as the Company can deliver disinfection/decontamination that Is highly effective (six log kill), fast-acting, and safe.

The Company’s SteraMist® products are designed to address a broad spectrum of industries using iHP™. TOMI’s operations consist of five main divisions based on its target industries: Hospital-HealthCare, Life Sciences, TOMI Service Network (TSN), Food Safety, and Commercial.

Image Source: Company

In other words, we find that TOMI’s products can be applied in several industries. Demand for disinfectants in all these industries is increasing at a rapid rate – hence, there is significant scope for the Company to generate customer interest and sales opportunities.

- Successful Business Model

The Company outsources the manufacturing and blending of the SteraMist® line of equipment and BIT™ Solutions. The SteraMist® equipment is manufactured by ISO9001-registered companies with multiple facilities in Pennsylvania, New York, New Jersey, North Carolina, California, and Australia. An EPA-approved blender blends the solution, including one (1) sole active ingredient, 7.8% Hydrogen Peroxide.

TOMI maintains ownership of all the SteraMist® product lines, including BIT™ Solution. Neither the manufacturer nor the chemical blender may modify the manufacturing or blending of products without TOMI’s request or consent in written format. TOMI maintains all creative control throughout the design and manufacturing process, which includes research & development through final product fabrication.

The approach mentioned above creates a capital-efficient infrastructure for the business. There is a steady stream of recurring revenue from sales of BIT solutions, while the razor/ razor blade model is a source of high margins for the Company.

However, the Company’s main attraction is its advantage over competitors. TOMI’s products can turn over space to an end-user far faster than its competition. The Company’s technology requires limited preparation for an area compared to competitors and does not rely on fans or any outside force to move throughout a space. The “iHP OH” is the smallest submicron 0.3-3-micron particle that receives a charge and can move around an area like a gas, going above, below, and beyond the hardest-to-reach places.

Another crucial and critical advantage is the technology’s superior material compatibility. iHP kills on contact and leaves no dangerous by-products in the treated areas.

Image Source: Company

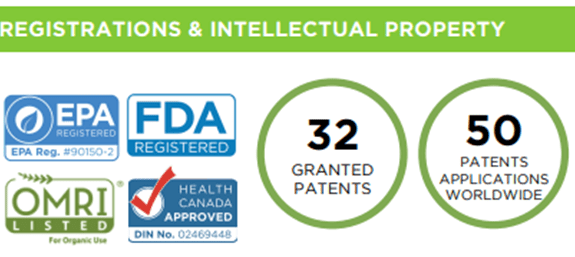

The Company protects its unique technology and products through obtaining United States and foreign patents. As part of its intellectual property protection strategy, TOMI has registered a BIT™ solution with the EPA, all fifty (50) United States states and multiple countries worldwide. The Company has received or is in the process of receiving Conformité Européene (CE) marks in the European Economic Area (EEA) and is approved by the Underwriters Laboratory (UL).

Image Source: Company

To summarize, the Company has created a promising business model – it provides an exclusive product that is much superior to those offered by competitors and protects its unique technology through multiple patents worldwide. Additionally, the business model is such that it provides a recurring revenue stream along with high margins and a capital-efficient infrastructure.

- Financial Performance

Of late, the Company has demonstrated a significant increase in revenues due to a rise in bookings and orders.

Image Source: Company

For Q2 FY23, TOMI recorded net revenue of $2,775,000 compared to $1,458,000 for Q2 FY22, representing an increase of $1,317,000 or 90%. The increase in revenue was primarily due to solid growth in product and service revenue in the current year period, as well as the internal team’s ability to execute and deliver two iHP SteraMist Custom Engineered Systems (CES) in the second quarter.

Specifically, TOMI recorded

Gross margin was 61% in Q2 FY23 compared to 63% in Q2 FY22. The decrease in gross profit was attributable to product mix in sales.

For Q2 FY23, Adjusted EBITDA was $2,000 compared to a loss of ($780,000) in the same prior year period. Net loss was ($89,000) or ($0.00) per basic and diluted share, compared to ($862,000) or ($0.04) per basic share.

Given TOMI’s current sales pipeline, the strength of its high-margin business model, and high incremental revenue profitability, management believes it may attain profitability in the fourth quarter.

For FY22, total net revenue was $2,812,000 compared to $2,010,000, an increase of $802,000, or 40% over FY21.

Recently, the Company added new distributors in North America and Europe and signed a contract with Vizient, the largest group purchasing organization (GPO) in the healthcare industry, supplying around $100 billion in annual member purchasing volume. Additionally, SteraMist technology was recognized as one of the Top 10 Infection Solution Providers of 2023 in the recent infection control solutions special edition.

All these indicate that TOMI’s management is diligently executing strategies to grow revenues, expand the sales network, and deliver improved results. In other words, given the Company’s recent financial performance, it seems that it has embarked on an upward trajectory.

Nevertheless, the Company does face the following risks:

Conclusion:

TOMI seems to have a promising future because of its unique and patented product offerings and increasing demand in target markets, as evidenced by its recent exponential revenue growth.

However, there are certain risks involved – the main ones being that the Company’s success is almost entirely dependent on the SteraMist brand, and broad acceptance of TOMI’s technology has not yet been achieved in specific crucial markets such as Hospital-Healthcare.

Thus, though TOMI seems to have strong fundamentals that will propel it toward growth, it would be best to proceed cautiously.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Click here to please visit our detailed disclosure

Reference:

https://feeds.issuerdirect.com/news-release.html?newsid=4566458402072920

https://feeds.issuerdirect.com/news-release.html?newsid=8544335451944174

https://irp.cdn-website.com/f78ba253/files/uploaded/TOMI%20STERAMIST.pdf

https://feeds.issuerdirect.com/news-release.html?newsid=7204907099705038

https://www.sec.gov/ix?doc=/Archives/edgar/data/314227/000165495423010755/tomz_10q.htm

https://www.sec.gov/ix?doc=/Archives/edgar/data/314227/000165495423006555/tomz_10q.htm

https://www.sec.gov/ix?doc=/Archives/edgar/data/314227/000165495423003029/tomz_10k.htm

No Comments