05 Jan EyePoint Pharmaceuticals: A Boon for Eye Disease Patients

EyePoint Pharmaceuticals, Inc. (NASDAQ: EYPT) develops and commercializes therapeutics to improve the lives of patients with severe eye disorders.

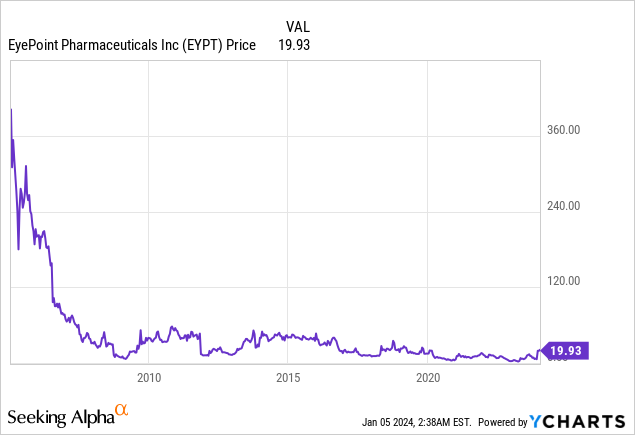

EyePoint Pharmaceuticals, Inc. (NASDAQ: EYPT)

Market Cap: $1.02B; Current Share Price: 19.93 USD

Data by YCharts

The Company and its Products

EyePoint’s pipeline leverages its proprietary Durasert® technology for sustained intraocular drug delivery, including delivery of EYP-1901, an investigational sustained intravitreal treatment currently in Phase 2 clinical trials. The proven Durasert drug delivery platform has been safely administered to thousands of patients’ eyes across four U.S. FDA-approved products, including YUTIQ®, for the treatment of posterior segment uveitis.

Image Source: Company

EYP-1901 is an investigational product and the Company’s lead pipeline program deploying a bioerodible Durasert insert of vorolanib, a selective and patented tyrosine kinase inhibitor (TKI), that potentially brings a new mechanism of action and treatment paradigm for serious eye diseases beyond existing anti-vascular endothelial growth factor (VEGF) large molecule therapies.

Image Source: Company

EYP-1901 is presently in Phase 2 clinical trials as a sustained delivery treatment for wet age-related macular degeneration (wet AMD), the leading cause of vision loss among people 50 years of age and older in the United States and non-proliferative diabetic retinopathy (NPDR), a largely untreated disease due to limitations of available therapies.

We’ll discuss the critical rationale for covering this Company.

- Vast Market Opportunity for Unique Product

EyePoint is focused on diseases affecting the posterior segment of the eye, with particular attention on retinal disease. The Company leverages best-in-class sustained delivery Durasert technology to achieve improved outcomes with more convenient dosing regimens. Diseases of the retina and posterior segment of the eye include wet age-related macular degeneration (AMD), diabetic retinopathy (DR), diabetic macular edema (DME), and other indications, including orphan diseases and certain cancers.

As the proportion of people in the U.S. age 65 and older grows more extensive, more people are developing age-related diseases such as AMD. From 2000-2010, the number of people with AMD grew 18 percent, from 1.75 million to 2.07 million. By 2050, the estimated number of people with AMD is expected to more than double from 2.07 million to 5.44 million. White Americans are expected to continue to account for the majority of cases. However, Hispanics are expected to account for the most significant rate of increase, with a nearly six-fold rise in the number of expected cases from 2010 to 2050.

Diabetic retinopathy (DR) is a frequent complication of diabetes mellitus. Slow but progressive changes in the retina’s tiny blood vessels may cause no symptoms or mild vision problems in the early stages. The disease progresses from NPDR to proliferative diabetic retinopathy (PDR). At any stage, retina bleeding and fluid accumulation lead to DME, which can cause blindness. Diabetes is the leading cause of new cases of blindness in adults. This is a growing problem as the number of people living with diabetes increases, and so does the number of people with impaired vision due to NPDR.

Image Source: Company

The lead pipeline program, EYP-1901, is initially focused on improving the treatment of wet AMD, DR, and DME, and these VEGF-mediated diseases share an underlying propensity to cause leakage from either pre-existing damaged blood vessels or new vessels (neovascularization) that, if untreated, can lead to severe visual loss.

These conditions are generally treated locally with frequent large-molecule anti-VEGF ligand-blocking intravitreal injections. While these treatments have a positive history of safety and initial efficacy, the need for frequent injections hampers long-term visual outcomes. Many patients with retinal or other posterior segment diseases, such as non-infectious uveitis, require lifelong treatment, and interruptions in therapy can result in disease reactivation and permanent visual loss. Accordingly, monthly or bi-monthly injections are not an effective long-term means of delivering a steady-state dose to the disease site for many patients. Finally, the risk of patient non-compliance increases when treatment involves multiple products or complex or painful dosing regimens, as patients age or suffer cognitive impairment or severe illness, or when the treatment is lengthy or expensive.

Drug delivery for treating ophthalmic diseases in the posterior segments of the eye is a significant challenge. Due to the effectiveness of the blood-eye barrier, it is difficult for systemically (orally or intravenously) administered drugs to reach the retina in sufficient quantities to have a beneficial effect without causing adverse side effects to other parts of the body.

Due to the drawbacks of frequent intravitreal injections, developing methods to deliver drugs to patients in a more precise, microdose zero-order release kinetics over more extended periods with Durasert can satisfy a significant unmet medical need for both patients and physicians. In addition, with less frequent injections, patients will be able to better comply with their prescribed treatment regimen as the burden of frequently going into the physician’s office for eye injections, usually over a lifetime after diagnosis, presents issues for patients.

Moreover, EyePoint has invested heavily in research and development. The Company’s pipeline represents multibillion-dollar product opportunities, as shown below.

Image Source: Company

Thus, EyePoint is uniquely positioned to provide improved medical treatment for the unmet needs of severe retinal disease patients globally. Hence, the Company may achieve increased revenues in the future.

- Financial Performance

For Q3 FY23, total net revenue was $15.2 million compared to $10.0 million for Q3 FY22. Net product revenue for Q3 FY23 was $0.8 million, compared to net product revenues for Q3 FY22 of $9.7 million. The decrease in net product revenue resulted from the sale of the YUTIQ franchise in May 2023 and the discontinuation of DEXYCU commercialization activities in 2023.

Net revenue from royalties and collaborations for Q3 FY23 totaled $14.4 million compared to $0.3 million in the corresponding period in FY22. The increase was primarily due to partial recognition of deferred revenue from the sale of the YUTIQ franchise, which will be recognized over two years in connection with the delivery of YUTIQ supply units.

The net loss for Q3 FY23 was $12.6 million, or ($0.33) per share, compared to a net loss of $18.4 million, or ($.49) per share, for the prior year.

On September 30, 2023, cash and investments totaled $136.0 million compared to $144.6 million on December 31, 2022.

For FY22, total net revenue was $41.4 million compared to $36.9 million for FY21. The net product revenue for FY22 was $39.9 million, compared to the net product revenues for FY21, which was $35.3 million.

Net revenue from royalties and collaborations for FY22 totaled $1.5 million compared to $1.6 million in FY21. Net loss was $102.3 million for FY22, or ($2.74) per share, compared to a net loss of $58.4 million, or ($2.03) per share, for FY21.

Outlook

EyePoint continued advancing EYP-1901 through clinical development in Q3 FY23, announcing positive masked safety results for its lead product candidate EYP-1901 in the ongoing DAVIO 2 and PAVIA Phase 2 clinical trials. The Company remains on track to report topline data for the DAVIO 2 trial in wet AMD in December 2023 and the PAVIA trial in non-proliferative diabetic retinopathy in the second quarter of 2024. EyePoint also plans to initiate the Phase 2 VERONA trial of EYP-1901 in diabetic macular edema in the first quarter of 2024.

Risks

EyePoint is laser-focused on its aim to improve the lives of patients suffering from retinal disease. It has several products in its pipeline that show great potential to achieve this goal. Nevertheless, the Company is exposed to certain risks.

Firstly, the Company has a history of losses and expects losses in the foreseeable future. Secondly, in the long run, EyePoint will need additional capital to fund its operations – if the Company cannot procure more funds, it may have to modify its business strategy.

Finally, the outcome of EyePoint’s clinical trials is uncertain, and any delay in the completion or termination of any clinical trial of product candidates could harm EyePoint’s business, financial condition, and prospects.

Conclusion

EyePoint is well-positioned to introduce various products to serve the unmet needs of patients suffering from severe eye diseases globally. The Company has already proved its mettle through its proven Durasert drug delivery platform, which has been safely administered to thousands of patients’ eyes across four U.S. FDA-approved products.

However, the Company has a history of losses, and the outcome of its clinical trials is uncertain – this, in turn, may impact its future revenues and profitability. Hence, potential investors must proceed with caution.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Click here to please visit our detailed disclosure

Reference:

https://investors.eyepointpharma.com/static-files/6292cff6-c871-4edd-8950-9a92e4a1e47f

https://www.sec.gov/ix?doc=/Archives/edgar/data/1314102/000095017023007180/eypt-20221231.htm

https://www.sec.gov/ix?doc=/Archives/edgar/data/1314102/000095017023058775/eypt-20230930.htm

Sorry, the comment form is closed at this time.